![]()

2024 Best F1 Exam Preparation Material with New Dumps Questions

Free F1 Exam Files Verified & Correct Answers Downloaded Instantly

CIMA F1 exam is an essential module for anyone looking to pursue a career in management accounting. By passing F1 exam, you will demonstrate your ability to report financial performance effectively, to manage working capital, to analyze financial risks, and to communicate financial information in a clear and concise manner. This module will provide you with the knowledge and skills you need to become a successful management accountant, and it will help you build a solid foundation for your future career.

CIMA F1: Financial Reporting exam is an essential certification for anyone seeking a career in finance, accounting or related fields. F1 exam evaluates candidates' knowledge and skills in financial reporting and analysis, providing a globally recognized credential that can enhance their career prospects. With the right preparation and study materials, candidates can pass the CIMA F1 exam and achieve their professional goals.

The CIMA F1 exam comprises of a three-hour assessment in which participants are required to answer 60 objective test questions. These questions explore areas such as interpretation of financial statements, preparation of financial statements, and international accounting standards (IAS). Furthermore, participants will be tested on their knowledge of the accounting framework and their ability to produce and evaluate financial statements.

NEW QUESTION # 43

UV's financial statements for the year ended 31 March 20X8 were approved for publication on 30 June

20X8.

In accordance with IAS 10 Events After the Reporting Period, which of the following material events would have been classified as a non-adjusting event in these financial statements?

- A. On 10 April 20X8 UV received a communication stating that one of its customers had ceased trading and gone into liquidation. The balance outstanding at 31 March 20X8 was unlikely to be paid.

- B. On 28 April 20X8 a fire destroyed half of UV's main production facility. Output was severely reduced for six months.

- C. On 1 June 20X8 UV was awarded damages of $70,000 in respect of a legal claim that it had made against the local government authority in October 20X7.

- D. On 1 June 20X8 UV's auditors discovered that an error in valuation had caused the closing inventory to be overvalued by $150,000.

Answer: B

NEW QUESTION # 44

Whilst undertaking an external audit, the auditor has identified that there is insufficient evidence to support the financial statements.

As a result the auditors consider these financial statements to be wholly unreliable for decision making purposes.

This will result in a modified audit report with the opinion being .

Answer:

Explanation:

NEW QUESTION # 45

Which of the following is a feature of a direct tax?

- A. It cannot be related to the individual circumstances of the tax payer.

- B. It is not levied on the eventual payer of the tax.

- C. It is levied on one part of the economy with the intention that it will be passed on to another.

- D. The formal incidence and effective incidence are usually the same.

Answer: D

NEW QUESTION # 46

The accounting profit before tax of an entity was $243,200 for the year ended 31 July 20X4.

The accounting profit included disallowable income from government grants of $48,000 and disallowable expenditure of $25,600 on entertaining expenses.

The entity also paid a $40,000 dividend to shareholders. The tax rates for the country were as follows:

Calculate the tax the entity is due to pay for the year ending 31 July 20X4.

- A. $39,174

- B. $47,840

- C. $57,546

- D. $44,160

Answer: B

NEW QUESTION # 47

Which THREE of the following are part of the International Accounting Standards Committee (IASC) Foundation structure?

- A. Standards Application Council

- B. International Financial Reporting Interpretations Committee

- C. International Financial Reporting Evaluations Committee

- D. International Organisation of Securities Commission

- E. Standards Advisory Council

- F. International Accounting Standards Board

Answer: B,E,F

NEW QUESTION # 48

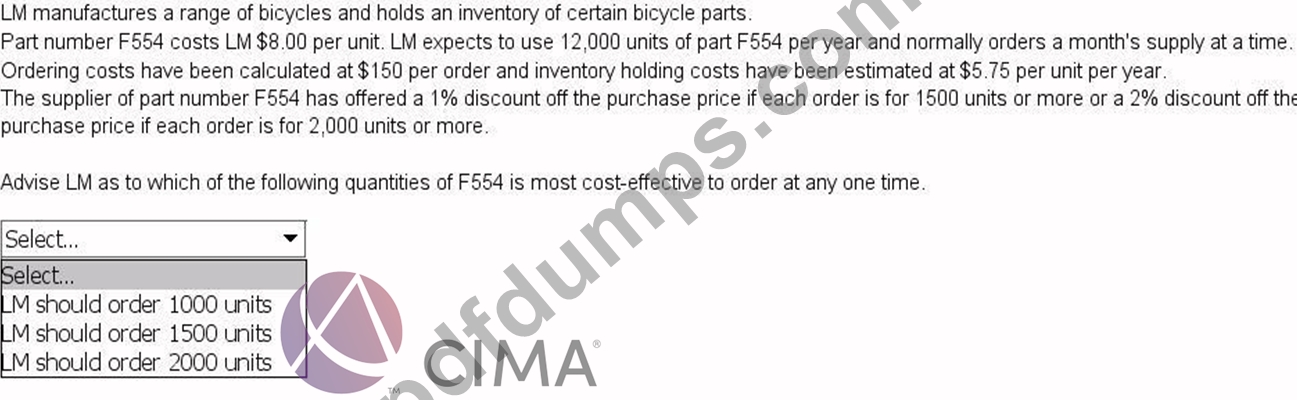

MN recently took out a 5 year term loan to buy raw materials to take advantage of a supplier's bulk discount that had been offered to them.

What approach to financing working capital has MN undertaken?

- A. Permanent

- B. Moderate

- C. Aggressive

- D. Conservative

Answer: D

NEW QUESTION # 49

A non-executive director of a company is somebody who:

- A. is involved in making operational decisions m the company

- B. does not earn remuneration from the company

- C. need not have experience of the industry in which the company operates

- D. can be appointed Chief Executive Officer of the company.

Answer: B

NEW QUESTION # 50

BBB has been experiencing liquidity problems and currently has an overdraft with the bank.

Which THREE of the following would be appropriate measures to help address this problem?

- A. Reduce the selling price of goods to reduce the holding of stock.

- B. Shorten the time taken to pay creditors.

- C. Invest in a short term deposit with the bank.

- D. Pay a dividend to shareholders.

- E. Offer early settlement discounts to encourage debtors to pay more quickly.

- F. Sell some surplus fixed assets.

Answer: A,E,F

NEW QUESTION # 51

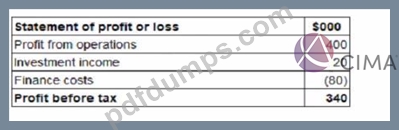

Below are extracts from LLL's financial statements for the year ended 31 December 20X2.

Depreciation of $25,000 was charged on properly, plant and equipment in the year and there were no disposals What is the cash generated from operations for inclusion in LLL's statement of cash flows for the year ended

31 December 20X2?

- A. $435,000

- B. $415,000

- C. $390,000

- D. $355 000

Answer: D

NEW QUESTION # 52

Which of the following is the most appropriate definition of the term 'factoring'?

- A. Where a business borrows a loan with short-term conditions from a third party

- B. Where a business is provided with a highly flexible regular source of short-term finance by a bank

- C. Where a business sells equity to third parties to gain short-term finance

- D. Where a business sells its accounts receivable to a third party at a discount

Answer: D

NEW QUESTION # 53

When calculating the gam chargeable to tax on the disposal of a building, which of the following would NOT be an allowable deduction?

- A. Interest on a loan that was used to assist with its original purchase.

- B. Costs of constructing an extension to the building.

- C. Legal fees arising on the original purchase of the building.

- D. Estate agent's fee payable on its sale.

Answer: A

NEW QUESTION # 54

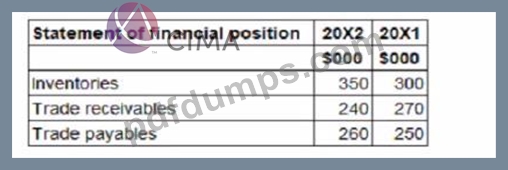

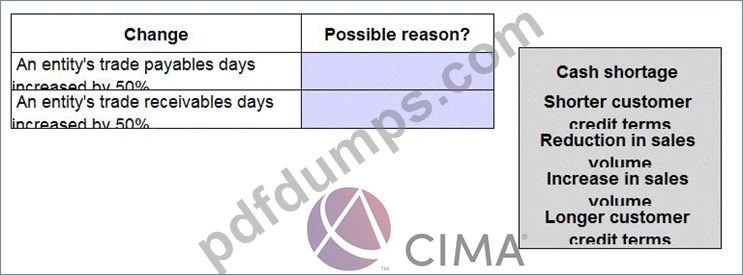

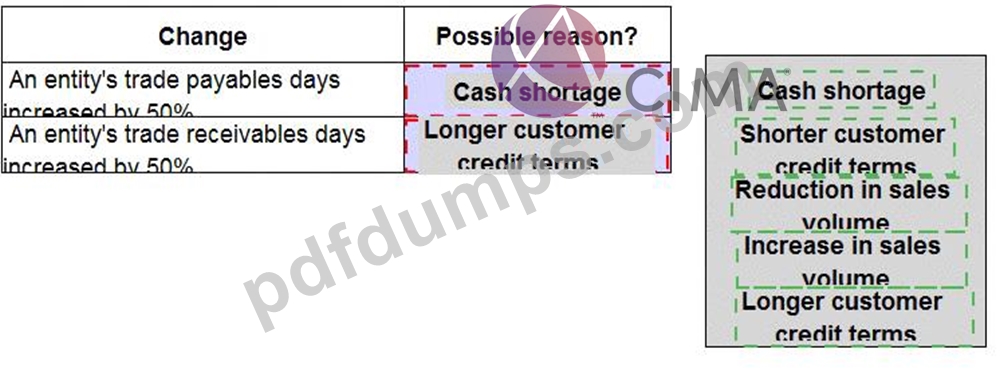

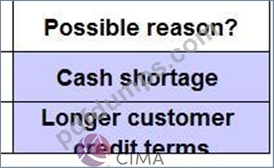

Indicate the possible reasons for the changes identified below to working capital ratios by placing the appropriate reason against each change.

Answer:

Explanation:

NEW QUESTION # 55

Which of the following is a feature of value added tax (VAT)?

- A. The value of all supplies must be taken into account when determining whether the registration threshold has been exceeded.

- B. Entities cannot register for VAT if the value of their taxable supplies is below the registration threshold.

- C. Only registered entities can charge VAT on sales or recover VAT paid on purchases.

- D. Entities that make only standard-rated or zero-rated supplies have their right to recover input tax restricted.

Answer: C

NEW QUESTION # 56

Answer:

Explanation:

NEW QUESTION # 57

From the list below identify the item that appears in the statement of financial position.

- A. The amount of interest charged on loans during the year.

- B. The amount of loans outstanding at the year end.

- C. The amount of interest actually paid during the year.

- D. The amount of loans repaid during the year.

Answer: B

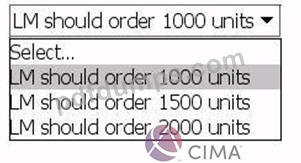

NEW QUESTION # 58

PZ has the following working capital ratios:

Which of the following could be the reason for the movements?

- A. A new credit controller has been employed who has been more rigorous with their collection procedure of receivables.

- B. The workforce of PZ have been on strike for a month during 20X1 but deliveries of inventory have still been received by the entity.

- C. PZ has implemented a just-in-time system of ordering inventory during 20X1.

- D. PZ has introduced a new policy to take discounts from suppliers during 20X1.

Answer: B

NEW QUESTION # 59

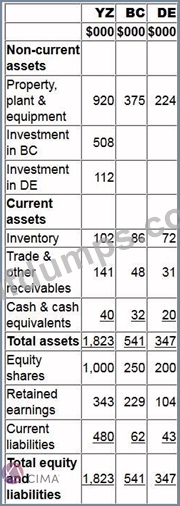

Statements of financial position for YZ, BC and DE at 31 March 20X2 include the following balances:

YZ purchased 90% of BC's equity shares for $508,000 on 1 January 20X2. On 1 January 20X2 BC's retained earnings were $183,000. YZ uses the proportion of net assets method to value non-controlling interest at acquisition.

YZ purchased 30% of DE's equity shares on 1 April 20X1 for $112,000. DE's retained earnings at 1 April

20X1 were $88,000.

On 1 February 20X2 YZ sold goods to BC for $28,000 at a mark up of 25% on cost. All the goods were still in BC's inventory at 31 March 20X2.

Calculate the value of the investment in associate to be recognised in the consolidated statement of financial position at 31 March 20X2.

Give your answer to nearest whole $.

Answer:

Explanation:

$116800

NEW QUESTION # 60

ST has an asset that was classified as held for sale at 30 June 20X4. The asset's carrying value was $230,000 and its fair value $210,000.

The cost of disposal was estimated to be $15,000.

In accordance with IFRS 5 Non-current Assets Held for Sale and Discontinued Operations, which of the following values should be used for the asset in the statement of financial position as at 30 June 20X4?

- A. $195,000

- B. $230,000

- C. $210,000

- D. $215,000

Answer: A

NEW QUESTION # 61

An asset cost $250,000 on 1 January 20X1 and on that date was assessed to have a residual value of

$40,000 and a useful economic life of six years. On 1 January 20X4 management assessed that the remaining useful economic life of the asset was five years and that the asset had a residual value of nil.

What is the depreciation charge for this asset in the year ended 31 December 20X4?

Give your answer to the nearest whole number.

Answer:

Explanation:

$29000

NEW QUESTION # 62

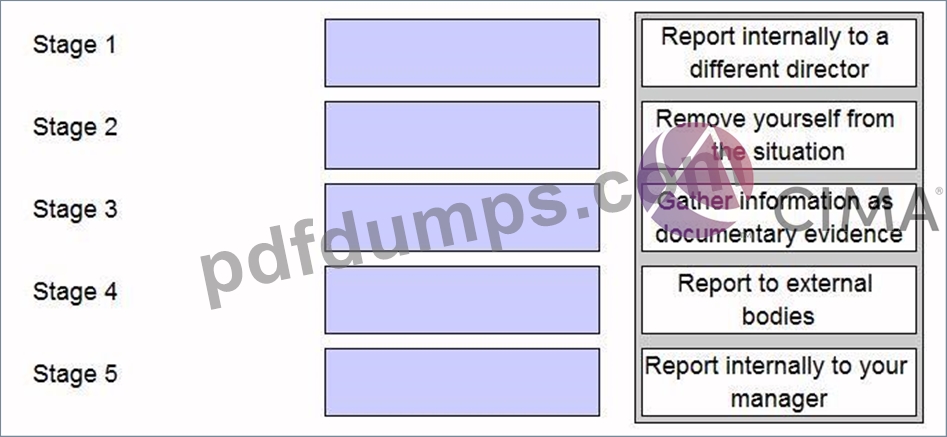

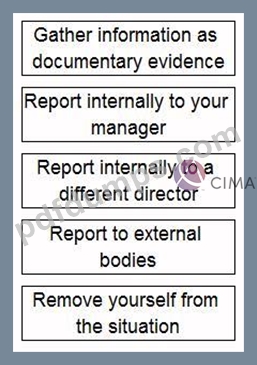

You work in the finance department of an entity. A director has approached you and asked you to falsify sales invoices which would significantly inflate revenue. The CIMA Code of Ethics suggests that you should deal with such an ethical dilemma by following a number of stages.

Place each of the stages identified below into chronological order.

Answer:

Explanation:

NEW QUESTION # 63

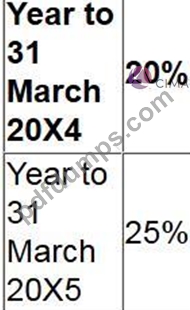

EFG prepares financial statements to 31 December each year. EFG has the following receivable days based on the year end receivable balances:

Which of the following would be a reason for this decrease in receivable days?

- A. EFG employed an inexperienced credit controller in November 20X2.

- B. EFG's revenue for 20X2 increased as a result of competitive pricing.

- C. EFG's largest customer negotiated an increase in credit terms during 20X2.

- D. EFG transferred collection of all receivables to a factoring agency during 20X2.

Answer: D

NEW QUESTION # 64

Which of the following would be classified as a parent and subsidiary relationship in accordance with IFRS 10 Consolidated Financial Statements?

- A. Entity D owns 25% of another entity's equity shares and associated voting rights and 100% of its preference shares.

- B. Entity C owns 45% of another entity's equity shares and can exercise significant influence over that entity's financial and operating policy decisions.

- C. Entity B owns 20% of another entity's equity shares and has an agreement with other equity shareholders of that entity that gives it power over a further 20% of the equity voting rights.

- D. Entity A owns 30% of another entity's equity shares and has the power to appoint or remove the majority of the members of the board of directors and control of the entity is through that board.

Answer: D

NEW QUESTION # 65

XYZ operates in Country A where tax rules state that entertaining costs and donations to political parties are disallowable for tax purposes.

XYZ calculated both its accounting and taxable profits for the year ended 31 December 20X2 after deducting $10,000 of entertaining costs.

It is considering what impact the ruling that "entertaining costs are disallowable for tax purposes" will have on its two profit figures.

Which of the following correctly states the impact of the ruling on the profits already calculated?

- A. Accounting profit will decrease by $10,000 and taxable profit will increase by $10,000.

- B. Both accounting and taxable profits will increase by $10,000.

- C. Accounting profit will not be affected but taxable profit will increase by $10,000.

- D. Both accounting and taxable profits will decrease by $10,000.

Answer: C

NEW QUESTION # 66

During the year a piece of equipment that originally cost $96,000, with accumulated depreciation of $39,000, met the criteria of IFRS 5 Non-current Assets Held for Sale and Discontinued Operations to be classified as held for sale.

The equipment is being advertised for sale at $46,000 and costs of $1,000 will be incurred to enable the sale to be completed.

At what value should the equipment be included in the statement of financial position at the year end assuming that it remains unsold?

Give your answer to the nearest whole number.

Answer:

Explanation:

$45000

NEW QUESTION # 67

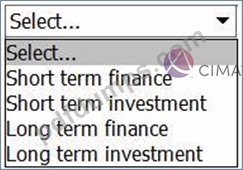

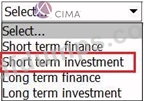

What is the correct classification of a 90-day government bond?

Answer:

Explanation:

NEW QUESTION # 68

......

Instant Download F1 Dumps Q&As Provide PDF&Test Engine: https://actualtorrent.pdfdumps.com/F1-valid-exam.html